MARKET

UPDATE AND COMMENTARY

December 20, 2015

After seven years, the Federal Reserve

finally raised their overnight lending rate a quarter of one percent Wednesday

afternoon (December 11th) and markets initially cheered the move with

US stock markets posting a three-day winning streak culminating Wednesday with

gains of about 1.5% in the major indexes.

Unfortunately, investor enthusiasm vanished on Thursday and Friday as

the major indexes gave back all of the gains early in the week to close the

week with very modest losses.

Time

Period

|

Dow

Jones

Industrial

Average

(DJIA)

|

S&P

500

|

Russell

2000

|

NASDAQ

|

1st Half

2015

|

-1.14%

|

+0.20%

|

+4.09%

|

+5.30%

|

Q3 2015

|

-7.58%

|

-6.94%

|

-12.22%

|

-7.35%

|

Q4 to Date

|

+5.18%

|

+4.45%

|

+1.85%

|

+6.56%

|

Week of Dec 14-

Dec 18

|

-0.79%

|

-0.34%

|

-0.23%

|

-0.21%

|

Year-to-Date

|

-3.90%

|

-2.59%

|

-6.95%

|

+3.95%

|

Source: The Wall Street Journal (Past performance is not

indicative of future returns). As of

market close December 18, 2015.

As the year draws to a close, I suspect

that most investors feel like 2015 has been a real let down after a couple of

good years of gains without much volatility.

My broad explanation of what has happened would necessarily begin with a

discussion about declining oil prices and the devastation of energy-related corporate

earnings. The necessary contraction by

energy companies in response to lost earnings has in turn spread over to other

sectors most notably the Materials and Industrials sector. As of December 18th, the

analytical company, FactSet, estimates that Energy sector earnings will decline

59% in 2015, followed by the Materials (-8%),

and the Industrials (-1%) sectors. The

losses from these three sectors will overwhelm those sectors that have posted

gains to result in an estimated combined decline in profits of -0.5% for

companies within the S&P 500 this year.

While International markets did just a bit

better last week, there has not been much to cheer about abroad in 2015 either.

Time

Period

|

Global

Dow xUS

|

STOXX

600

|

Dow

Jones

Devel

Mkt Region

Total

Stock Market

|

Dow

Jones

Emerg

Mkt Region

Total

Stock Market

|

1st Half

2015

|

+3.22%

|

+11.32%

|

+2.13%

|

+2.09%

|

Q3 2015

|

-12.60%

|

-8.80%

|

-9.09%

|

-19.33%

|

Q4 to Date

|

+2.05%

|

+3.87%

|

+3.11%

|

+1.34%

|

Week of Dec 14-

Dec 18

|

+0.37%

|

+1.53%

|

-0.23%

|

+2.42%

|

Year-to-Date

|

-7.94%

|

+5.46%

|

-4.26%

|

-16.54%

|

Source: The Wall Street Journal (Past performance is not

indicative of future returns). As of

market close December 18, 2015.

I continue to remain less than enthusiastic

about international markets primarily because Europe has shown no ability to

deal with the expansive government domination of most economies (high taxes,

low growth), the influx of refugees, and negative demographic trend (European

families are not reproducing enough children to replace the existing

population). Emerging markets are

suffering from bad governance, the collapse of the commodities markets, and a

strong US Dollar. China brings its own

set of issues as the leadership there continues to devalue the Yuan, provide

unreliable economic data to international investors, and I cannot shake the

feeling that they are building cities in which no one lives. Furthermore, I believe the Chinese economy is

extremely immature in that the government still has too much control over data

reported and tosses money managers it dislikes into jail to highlight just a

couple of problems. However, I believe

facts can change and lead to good investing opportunities. I will never exclude a market in the face of

building momentum, and I have only modestly cut my allocations to developed

markets abroad, but I have not made any new investments there either in the

past couple of months.

Oil is the most significant story in

commodities for the second year in a row.

After the price of a barrel of WTI Oil lost 46% in 2014, it is currently

down another 24% in 2015. I have already

discussed the impact this has had on earnings, but I also believe this

condition will not last indefinitely. As

oil prices have declined, US consumption has increased for the first time in a

number of years. Higher demand is a

natural product of cheaper prices.

Energy production will balance with demand and I believe oil prices will

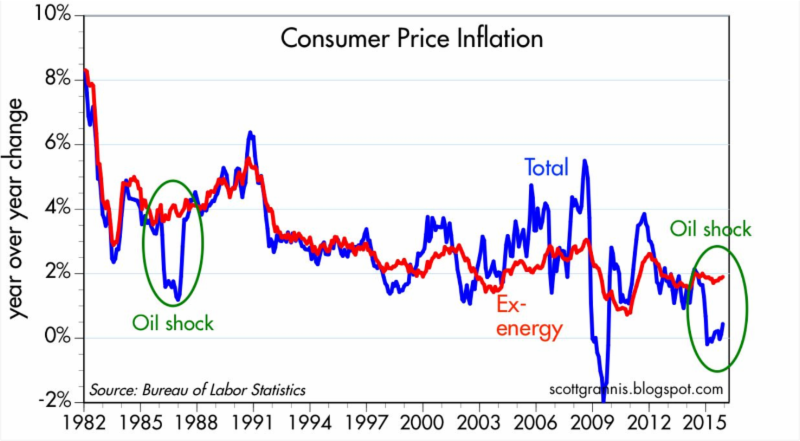

stabilize. When energy prices stabilize,

the threat of inflation will return because the decline in energy prices has

masked broader inflation in the economy.

Scott Grannis who writes the Calafia Beach Pundit created the chart

below to illustrate this point.

The blue line is reported inflation and the

red line shows what inflation is when the effects of energy prices are stripped

out of the calculation. When oil prices

collapsed back in 1986, you can see how inflation excluding energy maintained

its levels as it is doing today. Assuming

oil prices will find an equilibrium (which I believe they will), the mitigating

impact of falling oil prices will no longer be present and I would expect Total

Inflation (blue line) to return to about 2%.

More on this in the next section.

Before I discuss interest rates and the

bond asset category, I want to remind you that the Federal Reserve controls the

overnight lending rate between banks and the Federal Reserve. It does not control any other rates including

interest rates paid by the US Treasury on its bonds. Traders in the private sector determine all

other rates.

Interest rates in general increased

slightly last week. There has been much

financial media attention to the decline in interest rates Thursday and Friday,

however, I think it is impossible to determine the impact of the Federal

Reserve’s decision to raise the overnight lending rate simply on rates of

Treasuries in the days immediately following the Fed announcement. Until we see more inflation building into the

economy and improving economic growth statistics, I do not believe there will

be much change in rates for the short-term.

The real news in the bond world has focused

on the high-yield bond sector.

High-yield bonds have seen some negative volatility in the past couple

of weeks due to concerns of diminished liquidity (not enough buyers as sellers

enter into the market). Again, much of

the story centers on the energy sector because low oil prices have hurt cash

flows of many smaller companies and fears are increasing that default rates

will increase in the coming months. One

high yield fund manager, Third Avenue Management LLC, suspended redemptions

because they could not sell their positions fast enough to meet cash requests. This announcement sent nervous investors

across the entire sector to the exits hurting many different high-yield

managers. Morningstar®

reports that the high-yield sector has declined 3.5% over the past month and is

now down 4.8% for the year ranking the sector 15th out of the 16 taxable

bond sectors Morningstar® ranks.

Nine other taxable bond sectors are negative as well leaving bond

investors in the same circumstance as stock investors for 2015 facing negative

returns for the first time in a number of years. If you believe that 2016 will be a better

year than 2015, and that energy prices will stabilize as I do, then I believe

the recent sell-off in the high yield bond sector is oversold. However, I will continue to watch this bond

sector very closely going forward.

MORE

ON ENERGY, THE ECONOMY, AND THE FED

Investors cannot look at events in isolation;

the world just doesn’t work that way.

The old kids song, “Dem Bones” that teaches children “the foot bone is

connected to the ankle bone, and the ankle bone is connected to the leg bone,”

and so on is what comes to my mind when I think about how nearly everything is interconnected

in the 21st century and how 2015 evolved.

Oil is a commodity and as such the value of

a barrel of oil is very dependent on supply and demand—economics 101. The more supply you have of something

compared to demand the price will fall.

The opposite is true as well. For

years, the Organization of Petroleum Producing States (OPEC) set the price of

oil by colluding to set production levels to maintain acceptable (to OPEC) oil

prices. As US production of oil

decreased, the US became the world’s largest importer of oil and was thus

vulnerable to OPEC. As a response to the

Arab-Israeli War in 1973, OPEC stopped exporting oil to the United States. This quadrupled the price oil in just a

matter of months. By 1974, gas lines

were common throughout the United States, and OPEC’s power helped push the

United States and Israel to negotiate a settlement with the Arabs that was much

more favorable to the Arabs then would have otherwise happened. In the years following, Saudi Arabia willed

OPEC to maintain oil prices at levels they determined. The cartel worked well until 1986 when Saudi

Arabia decided to punish non-complying OPEC members who ignored quotas by

pumping as much oil as possible, the price of oil plummeted, and the Saudi’s

made their point.

As it has turned out, the 1986 period was

just a precursor of things to come.

Since the mid-1970’s the rest of the world made efforts to break OPEC’s

stranglehold on oil production and prices.

Oil production began or was expanded in countries like Mexico and

Brazil, and exploration began in inhospitable areas like the North Sea and

Alaska. The US passed fuel mileage

legislation and over time, we have become a significantly more fuel-efficient

country. The domination of OPEC on the

world has been broken. However, the Saudi’s

ability to pump large amounts of oil and push the price of oil down has

contributed to the 65% decline in WTI Oil since the end of 2013. The motivation of Saudi Arabia today is much

the same as it was in 1986 and that is to maintain its market share.

The United States has experienced a

revolutionary growth in oil production primarily due to giant technological advances. Proven oil reserves (reachable with current technology) make the US

the largest potential oil producer in the world dwarfing Saudi Arabia. In terms of natural gas, the US has proven

reserves that can last for 700 years.

These facts, I believe, should have a significant positive impact on

life in the US economically and geopolitically.

However, the rapid decline in oil prices has caused short-term

disruptions and I believe we are witnessing the impact of these disruptions

including shutting down rigs, loss of jobs, diminished economic growth in

supporting industries, and the possible bankruptcy of fringe producers. As a practical matter, high-yield bond

investments in this sector and related sectors may suffer a spike in defaults

as the weaker players exit. I believe

these issues are behind much of the recent turbulence in the stock market and

the chart below shows the loose correlation between percentage changes in the

AMEX Oil Index (blue line) and the S&P 500 Index (orange line).

Longer-term, however, I believe the energy

sector will adapt, adjust, and profit. I

cannot stress enough the importance new technology has had in driving down

production costs. I have read that the

newest rigs are producing oil for as low as $29 per barrel. This allows oil companies to be profitable at

far lower prices than previously thought.

With the United States resuming its place as the largest producer of oil

in the world (and if oil exports are once again permitted), the power of OPEC

will continue to diminish and I believe oil prices will stabilize.

Longer-term, however, I believe the energy

sector will adapt, adjust, and profit. I

cannot stress enough the importance new technology has had in driving down

production costs. I have read that the

newest rigs are producing oil for as low as $29 per barrel. This allows oil companies to be profitable at

far lower prices than previously thought.

With the United States resuming its place as the largest producer of oil

in the world (and if oil exports are once again permitted), the power of OPEC

will continue to diminish and I believe oil prices will stabilize.

What happens when energy prices stabilize? Scott Grannis estimates that the bond market

is pricing in an inflation rate of just 1.25% over the next five years, considerably

below the approximately 2% ex-energy inflation rate currently estimated to be

in the economy today. The connection

between stable oil prices and an increase in inflation could force the bond

market to re-price bonds down to account for higher inflation should it

materialize. Higher inflation could also

lead the Federal Reserve to reevaluate the pace at which it raises interest

rates. Right now markets are generally

expecting the Fed to move in a very deliberate (slow) pace in an effort to

avoid the kind of shocks on the economy that investors dislike. However, if inflation gets going, the Fed may

have to move faster than what investors are thinking and I believe that may be

problematic much as the unexpected size of price declines disrupted the energy

sector. Oil was an important story in

2015 and I believe it will be again in 2016.

LOOKING

AHEAD

The year is limping to an

unimpressive end. Many will soon be

turning their attention to 2016 and what prospects the new year will

bring. I will address 2016 in an

upcoming Update, but for now let’s focus on the near-term.

Most of you are now

familiar with the Dorsey Wright & Associates Daily Asset Level Indicator

(DALI) chart below.

As of December 20, 2015. Source: DorseyWright & Associates.

This chart outlines the most

basic relative strength relationship between the six major asset categories. Since my last Update, there has been no change

in the order of the six major asset categories, but there has been some changes

to the underlying tally scores of each.

Domestic Equities is unchanged both in terms of being the strongest

category and with a tally rank of 341.

Fixed Income (bonds) remains number two, but its tally score fell from

238 to 232 meaning other major asset categories have strengthened slightly at

the expense of Fixed Income. Cash, the

money market sector, tally increased from 205 to 211. International Equities added 3, Currency fell

by 1, and Commodities added 4. These

small changes are notable only for looking at the subtle changes underway in

the markets, however, there is nothing to suggest the need to make any major

adjustments to your portfolios.

As I discussed earlier,

the drop in the High-yield bond sector is notable. If you have a short time horizon the weakness

is important and may justify some changes, however, if you are a long-term

investor, I do not believe wholesale changes in your fixed income allocations

are necessary at this time. However,

further weakness may cause me to change this view. The High-yield sector must be watched closely. The Fed’s raising interest rates a quarter

percent will not, in my view, ease the challenge for investors who require

income beyond the meager interest earned on CDs or money market funds.

One additional comment on the fixed income sector. I mentioned earlier that the fixed income asset category in general has been a disapointment in 2015 with negligible returns at best and a couple of percentage point drop at worst. As we enter 2016 I am searching for signs to see if 2016 will be any better. So far I have not found that evidence. More on this in future Updates as well.

This will be my last

Update for 2015. I hope you and your

family have a warm, loving, and happy holiday season.

Paul L. Merritt,

MBA, C(k)P®, AIF®, CRPC®

Principal

NTrust Wealth

Management

P.S.

If you think this type of analysis would be of benefit to anyone you know,

please share this communication with them.

Past performance is not indicative of future results and there is no

assurance that any forecasts mentioned in this report will be obtained.

Technical analysis is just one form of analysis. You may also want to

consider quantitative and fundamental analysis before making any investment

decisions.

All indices are

unmanaged and are not available for direct investment by the public. Past

performance is not indicative of future results. The S&P 500 is based on the average

performance of the 500 industrial stocks monitored by Standard & Poors and

is a capitalization-weighted index meaning the larger companies have a larger

weighting of the index. The S&P 500

Equal Weighted Index is determined by giving each company in the index an equal

weighting to each of the 500 companies that comprise the index. The Dow

Jones Industrial Average is based on the average performance of 30 large U.S.

companies monitored by Dow Jones & Company.

The Russell 2000 Index Is comprised of the 2000 smallest companies of

the Russell 3000 Index, which is comprised of the 3000 biggest companies in the

US. The NASDAQ Composite Index (NASDAQ)

is an index representing the securities traded on the NASDAQ stock market and

is comprised of over 3000 issues. It has

a heavy bias towards technology and growth stocks. The STOXX® Europe 600 is derived

from the STOXX Europe Total Market Index (TMI) and is a subset of the STOXX

Global 1800 Index. With a fixed number

of 600 components, the STOXX Europe 600 represents large, mid, and small capitalization

countries of the European region. The

Dow Jones Global ex-US index represents 77 countries and covers more than 98% of the world's

market capitalization. A full complement of sub indices, measuring both sectors

and stock-size segments, are calculated for each country and region.

Information in this update has been obtained from and is based upon

sources that NTrust Wealth Management (NTWM) believes to be reliable; however,

NTWM does not guarantee its accuracy. All opinions and estimates constitute

NTWM's judgment as of the date the update was created and are subject to change

without notice. This update is for informational purposes only and is not

intended as an offer or solicitation for the purchase or sale of a security.

Any decision to purchase securities must take into account existing public

information on such security or any registered prospectus.

Emerging market investments

involve higher risks than investments from developed countries and involve

increased risks due to differences in accounting methods, foreign taxation,

political instability, and currency fluctuation. The main risks of

international investing are currency fluctuations, differences in accounting

methods, foreign taxation, economic, political, or financial instability, and

lack of timely or reliable information or unfavorable political or legal

developments.

The commodities industries can be significantly affected by

commodity prices, world events, import controls, worldwide competition,

government regulations, and economic conditions. Past performance is no

guarantee of future results. These investments may not be suitable for all

investors, and there is no guarantee that any investment will be able to sell

for a profit in the future. The Dow

Jones UBS Commodities Index is composed of futures contracts on physical

commodities. This index aims to provide

a broadly diversified representation of commodity markets as an asset

class. The index represents 19

commodities, which are weighted to account for economic significance and market

liquidity. This index cannot be traded

directly. The CBOE Volatility Index - more commonly referred to as

"VIX" - is an up-to-the-minute market estimate of expected volatility

that is calculated by using real-time S&P 500® Index (SPX) option

bid/ask quotes. VIX uses nearby and second nearby options with at least 8 days

left to expiration and then weights them to yield a constant, 30-day measure of

the expected volatility of the S&P 500 Index.

TIPS are U.S. government securities designed to protect investors

and the future value of their fixed-income investments from the adverse effects

of inflation. Using the Consumer Price Index (CPI) as a guide, the value of the

bond's principal is adjusted upward to keep pace with inflation. Increase in

real interest rates can cause the price of inflation-protected debt securities

to decrease. Interest payments on

inflation-protected debt securities can be unpredictable.

The NYCE US Dollar Index is a

measure that calculates the value of the US dollar through a basket of six

currencies, the Euro, the Japanese Yen, the British Pound, the Canadian Dollar,

the Swedish Krona, and the Swiss franc.

The Euro is the predominant currency making up about 57% of the basket.

Currencies and futures generally

are volatile and are not suitable for all investors. Investment in foreign exchange related

products is subject to many factors that contribute to or increase volatility,

such as national debt levels and trade deficits, changes in domestic and

foreign interest rates, and investors’ expectations concerning interest rates,

currency exchange rates and global or regional political, economic or financial

events and situations.

Corporate bonds contain elements

of both interest rate risk and credit risk. Treasury bills are guaranteed by

the U.S. government as to the timely payment of principal and interest, and if

held to maturity, offer a fixed rate of return and fixed principal value. U.S.

Treasury bills do not eliminate market risk. The purchase of bonds is subject

to availability and market conditions. There is an inverse relationship between

the price of bonds and the yield: when price goes up, yield goes down, and vice

versa. Market risk is a consideration if sold or redeemed prior to maturity.

Some bonds have call features that may affect income.

The bullish percent indicator (BPI) is a market breath

indicator. The indicator is calculated by taking the total number of

issues in an index or industry that are generating point and figure buy signals

and dividing it by the total number of stocks in that group. The basic

rule for using the bullish percent index is that when the BPI is above 70%, the

market is overbought, and conversely when the indicator is below 30%, the market

is oversold. The most popular BPI is the NYSE Bullish Percent Index,

which is the tool of choice for famed point and figure analyst, Thomas Dorsey.