2016

MARKET OUTLOOK AND COMMENTARY

January 10, 2016

After an unsatisfying 2015, markets both

here and abroad ushered in the New Year with a sharp sell-off. You can see below that the key indexes fell

between 6% and 8% in just 5 trading days.

For those who are historians, both the Dow Jones Industrial Average and

S&P 500 had their worst first week performance of a year ever. Ouch.

|

Time

Period

|

Dow

Jones

Industrial

Average

(DJIA)

|

S&P

500

|

Russell

2000

|

NASDAQ

|

|

2015

|

-2.23%

|

-0.73%

|

-5.19%

|

5.73%

|

|

Week 1, 2016

|

-6.19%

|

-5.96%

|

-7.90%

|

-7.26%

|

Source: The Wall Street Journal (Past performance is not

indicative of future returns). As of

market close January 8, 2016.

International markets shared in the selloff

as well with most global indexes down around 6%. China suffered the most with the Shanghai

Composite losing 10%.

|

Time

Period

|

Global

Dow xUS

|

STOXX

600

|

Dow

Jones

Devel

Mkt Region

Total

Stock Market

|

Dow

Jones

Emerg

Mkt Region

Total

Stock Market

|

|

2015

|

-6.63%

|

6.79%

|

-2.59%

|

-15.86%

|

|

Week 1, 2016

|

-6.10%

|

-6.69%

|

-6.06%

|

-6.24%

|

Source: The Wall Street Journal (Past performance is not

indicative of future returns). As of

market close January 8, 2016.

The 5-day decline of 6% in the S&P 500

this past week is eerily similar to the 11% 6-day decline in the S&P 500

from August 18th to August 25th last summer. Now as then, most analysts and commentators

place much of the responsibility squarely on the back of China and that country’s

slowing economy and weakening currency.

Similarly, oil prices fell 10.5% last week compared to 9.6% over the

six-day stretch last August. What is new

this time around is the Federal Reserve has raised interest rates a quarter of

a percent, and I would argue the geopolitical threat from terror has increased.

A fair question to ask is whether US

investors should be worried about a Chinese slowdown. I will address this topic and my outlook for

2016 in the next section.

Before turning my attention to 2016, I

would like to do a quick look back to some 2015 data.

The best performing sector in 2015 was Health

Care with a nearly 6% gain followed by Consumer Discretionary (+4.8%) and

Information Technology (+3.6). Energy

(-25.5%) was the worst performing sector by far followed by Materials (-12.3%)

and Utilities (-8.2%). Avoiding or under-weighting

these sectors was important for portfolio performance in such a lackluster

year.

The Federal Reserve raised interest rates

for the first time in seven years increasing the overnight lending rate by a

quarter percent (25 basis points) the third week in December. Speculation about the Fed’s move was one of

the dominant topics in 2015, yet after the move, little changed. Interest rates finished the year marginally

higher in a year when rates meandered about.

The benchmark 10-year US Treasury closed up 0.1% to 2.27%. The Bond asset category was a disappointment

in 2015. The Barclays US Aggregate Bond

index was up just 0.6% and only five of the sixteen taxable bond sectors

tracked by Morningstar® were positive in 2015. The best performing taxable bond sectors were

Preferred Stocks (+3.2%), Intermediate Government (+0.4%), and Short-Term Bond

(+0.2%). The worst performing sectors

were Emerging Markets Bond (-6.0%), World Bond (-4.1%), and High Yield (-4.0%).

The US Dollar continued to gain in strength

in 2015. The US Dollar index, a

comparison of the US Dollar against a basket of the other major currencies,

gained 9.3% in 2015. The US Dollar was

up 10.3% against the Euro and up nearly 1% to the Japanese Yen. The impact of a stronger US Dollar helped

contribute to lower US corporate earnings, poor international stock and bond

performance at home, and a decrease in demand for oil overseas. Currency fluctuations play an important role

in global economics and I believe will continue to do so in 2016.

OUTLOOK

FOR 2016

Early last year (January 25, 2015) I talked

about four big themes to watch in 2015:

Greece, the US Federal Reserve raising interest rates, geopolitical

risks abroad, and the uncertainty surrounding US domestic politics. While Greece created all sorts of trouble for

the markets early in the year, the Europeans managed to stabilize the European

Union. The Fed did raise rates a quarter

percent at their last meeting in 2015 and the sun still came up the next

day. Geopolitical challenges came and

went. Terror attacks continued and

stability in the Middle East deteriorated without significant impact on markets. However, oil prices fell during the political

turmoil in the Middle East and that is a new twist on global economics. Finally, my prediction that growth-oriented

policies coming from Congress would be minimal has unfortunately turned out to

be true.

While I did not feel like the economy was

likely to grow at a rate greater than 2.5% in 2015, I thought equity returns

would be better than they were. I

believe that the energy sector was responsible for much of what has challenged

markets. However, I also believe that

the anti-growth fiscal policies via law and rulemaking, has much responsibility

for lackluster growth as well. Finally,

a stronger US Dollar has diminished earnings of US companies that have large

overseas earnings.

My outlook for 2016 is MORE OF THE SAME

resulting in lackluster economic growth (less than 2.5% real gross domestic product

(GDP), more volatility in the markets, and equity returns that fail to exceed

the 8.5% average annual return of the S&P 500 since 1980. I believe it would be a great year if we did

meet that 36-year average, but I am not optimistic thinking we will fall

somewhat short—something that has happened about four times every ten years

since 1980.

Let me say upfront that I do not have a

crystal ball or some magical powers to predict the future. In fact, I have felt for years making

predictions was a fool’s errand.

However, I do believe that it is very necessary to have some expectation

about the near future to properly position portfolios. Let me offer my rationale for why I think

next year will look much like this year.

1)

All the actors on the global stage

are the same. The political and economic

leaders are unchanged and are not expected to change in 2016 (clearly 2017 may

be a different story). We know what

President Obama thinks about US economic policy, what Ms. Yellen thinks about monetary

policy, what Ms. Merkel thinks about the European Union (EU), and so on.

2)

Going into the November presidential

elections there will be no improvement in fiscal policies coming from

Congress. I do believe there remains

more downside risk in Washington as President Obama tries to maximize the

regulatory legacy of his administration in his last year.

3)

Corporate earnings and revenue

growth have been slowing. Corporate

earnings is the food that feeds the market and without earnings growth, markets

will struggle, in my view.

4)

Oil prices will continue to struggle

to find equilibrium. Even if oil prices

do stabilize, I believe they will be lower than they have been over the past

decade for the near future.

Here are some of the key themes and issues

I anticipate will be important in 2016:

I believe that oil prices will stabilize. I do not know where that point of

stabilization will occur, but I do believe it will. This is how commodity markets have always

worked. I do believe the price will stabilize closer

to $32/barrel than $95/barrel of our recent past. I continue to believe that low oil prices are

a great benefit for most of the economy, but clearly, the energy sector is

under a great deal of stress. The United

States has the potential to become the world’s greatest oil producer but has a

long way to go even as oil exports have been permitted for the first time in

over 40 years. Energy prices will

continue to be a key issue in 2016.

The Federal Reserve will remain in the forefront of

investors’ minds.

After getting the first rate hike accomplished last year, the discussion

will now turn to the frequency and magnitude of future rate hikes. The Fed must

walk a very tight balance between normalizing rates while not harming a

sputtering economy or reacting too late to prevent an inflation surge. Markets are currently predicting two

additional 0.25% rate hikes this year and next.

Where would the financial media be these days if they did not have the

Federal Reserve to worry about?

Interest rates should continue their upward trajectory;

however, there are many factors that influence interest rates including the

Fed, inflation, and economic growth.

Interest rates have historically been the most difficult to predict and

the past few years have been no different.

Rising interest rates need economic growth and some degree of inflation

to move upwards. I believe real economic

growth will continue to run below 2.5%, so for rates to rise considerably

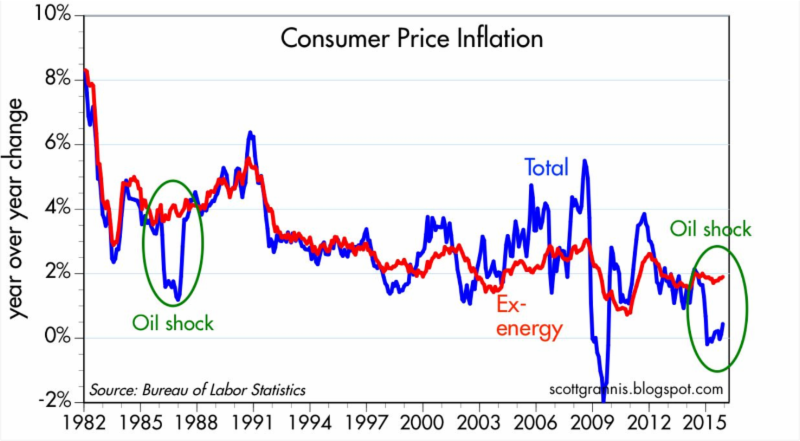

higher than where they are today, I think inflation will need to tick up. Inflation, in my view, will remain subdued;

however, if oil prices stabilize, there may be an uptick in inflationary

pressure. I discussed this issue in some detail in my December 20, 2015 Update. If inflation speeds up, the Fed may have to

pick up the frequency and possibly the magnitude of their rate increases which

may in turn put additional pressure on bonds.

The Bond asset category will continue to struggle

in my view. Rising interest rates,

uncertainty in the lower quality bond sectors, and the Fed’s monetary policy

all point to a similar weak performance like we saw in 2015. Higher yields will continue to come from

higher-risk assets that may be prone to periodic selloffs.

The US Dollar will continue to strengthen in 2016—just

not as fast. The currency market is the

largest capital market in the world with average trading volume in excess of $5

trillion each and every day. The free

flow of cash around the world is instrumental in orderly global trade, but it

is also an indicator of the strength or weakness of a country or region. Currencies trade like commodities and are

subject to the same supply/demand issues that affect the price. The US Dollar has been in demand because

traders have believed interest rates on US Treasuries will continue to increase

compared to other nation’s bonds, and because the security of US Treasuries is

second to none. Traders who fear the geopolitical

turbulence frequently turn to US Treasuries thus increasing demand for the US

Dollar.

European growth will continue to lag the US. I have little confidence that developed

European countries will be able to grow at levels close to or better than the

US. Europe is the US on steroids in

terms of over-taxation, government regulation, and wealth transfer

payments. All of this gives me little

reason to be optimistic about growth in developed Europe even as the European

Central Bank (ECB) continues with its quantitative easing program. Eastern Europe, if allowed to act independently

of either the European Union or Russia could offer excellent investment

opportunities. However, this is a big

if. I believe Emerging markets will

continue to struggle under the challenges of a stronger US Dollar and weakening

demand from China. As I have said

recently, I am not ignoring international investing; I am just suggesting there

are some serious headwinds to investment there now.

I believe volatility will increase

due to the Fed’s desire to return to more normal monetary policies. We have benefited since the 2008 recession by

Fed policies that indirectly helped dampen volatility, and that has been a

great thing for investors. I do not know

a single investor that enjoys volatility, but most accept this as the price to

be paid to be a long-term investor.

Finally, I fear that acts of terror will continue in

2016. As the world adapts to

this new reality, I do not believe markets will over-react to such events

provided they are isolated and have minimal impact on economic activity.

LOOKING

AHEAD

Although I do not believe

2016 will be a great year, I do believe the US economy is not going to fall off

a cliff. We appear to be in a

transitional year. After years of near

zero interest rates from the Fed, we may well be for a period of rate

increases, albiet small ones. Leadership

in the White House will certainly change in early 2017, but to who we have no

idea. From an investment perspective, I

hope that the next President and Congress can do more to help growth than has

been the case for so many years.

The S&P 500 is

currently 71% oversold. Traditionally,

when markets become more than 100% oversold it becomes an attractive point of

entry. Another important signal I watch,

the New York Stock Exchange Bullish Percent (NYSEBP) is an indicator of what I

consider the overall riskiness in the market.

The current reading is 28 and I consider anything below 30 to be

generally less risky going forward. For

perspective, the NYSEBP reached down to 26 last August during the first China

related selloff, and to 18 during the last major correction in the fall of

2011.

Most of you are now

familiar with the Dorsey Wright & Associates Daily Asset Level Indicator (DALI)

chart below.

As of January 11, 2016.

Source: DorseyWright & Associates.

This chart outlines the

most basic relative strength relationship between the six major asset

categories. Since my last Update, there

has been no change in the order of the six major asset categories, but there

has been some changes to the underlying tally scores of each. Domestic Equities has shown some weakness

falling from 341 to 323 since my December 20th Update. The numbers indicate that weakness in the

small capitalization sectors is responsible for much of the decline. Fixed Income (bonds) remains number two and

has improved as has Cash (Money Market sector).

Currencies and Commodities have also improved although the Commodity

asset category remains firmly in last place.

International Equities weakened by the continuing struggles of the

emerging market sectors.

The high yield bond

sector’s struggles will conintue in 2016 primarily because of the energy sector,

and the year will yet another mediocre year for bonds in general. The best bond sectors at the start of the

year are high credit quality and municipals.

I think the floating-rate (bank loan) sector is oversold enough to find

the values compelling along with their good yields.

I believe commercial real

estate could provide positive returns as supply continues to lag demand and is

a sector I am evaluating.

I cannot stress enough that the weak start in 2016 is just that, a weak start. Volatility is the price you pay to be an investor. There are 51 more trading weeks remaining in the year and while I believe this will be a below trend year for equity returns, I do think markets will be positive for 2016.

I hope all of you had a

very Happy New Year and cheers to your happiness, health, and prosperity!

Paul L. Merritt,

MBA, C(k)P®, AIF®, CRPC®

Principal

NTrust Wealth

Management

P.S.

If you think this type of analysis would be of benefit to anyone you know,

please share this communication with them.

Past performance is not indicative of future results and there is no

assurance that any forecasts mentioned in this report will be obtained.

Technical analysis is just one form of analysis. You may also want to

consider quantitative and fundamental analysis before making any investment

decisions.

All indices are

unmanaged and are not available for direct investment by the public. Past

performance is not indicative of future results. The S&P 500 is based on the average

performance of the 500 industrial stocks monitored by Standard & Poors and

is a capitalization-weighted index meaning the larger companies have a larger

weighting of the index. The S&P 500

Equal Weighted Index is determined by giving each company in the index an equal

weighting to each of the 500 companies that comprise the index. The Dow

Jones Industrial Average is based on the average performance of 30 large U.S.

companies monitored by Dow Jones & Company.

The Russell 2000 Index Is comprised of the 2000 smallest companies of

the Russell 3000 Index, which is comprised of the 3000 biggest companies in the

US. The NASDAQ Composite Index (NASDAQ)

is an index representing the securities traded on the NASDAQ stock market and

is comprised of over 3000 issues. It has

a heavy bias towards technology and growth stocks. The STOXX® Europe 600 is derived

from the STOXX Europe Total Market Index (TMI) and is a subset of the STOXX

Global 1800 Index. With a fixed number

of 600 components, the STOXX Europe 600 represents large, mid, and small

capitalization countries of the European region. The Dow Jones Global ex-US index represents 77 countries and

covers more than 98% of the world's market capitalization. A full complement of

sub indices, measuring both sectors and stock-size segments, are calculated for

each country and region.

Information in this update has been obtained from and is based upon

sources that NTrust Wealth Management (NTWM) believes to be reliable; however,

NTWM does not guarantee its accuracy. All opinions and estimates constitute

NTWM's judgment as of the date the update was created and are subject to change

without notice. This update is for informational purposes only and is not

intended as an offer or solicitation for the purchase or sale of a security.

Any decision to purchase securities must take into account existing public

information on such security or any registered prospectus.

Emerging market investments

involve higher risks than investments from developed countries and involve

increased risks due to differences in accounting methods, foreign taxation,

political instability, and currency fluctuation. The main risks of

international investing are currency fluctuations, differences in accounting

methods, foreign taxation, economic, political, or financial instability, and

lack of timely or reliable information or unfavorable political or legal

developments.

The commodities industries can be significantly affected by

commodity prices, world events, import controls, worldwide competition,

government regulations, and economic conditions. Past performance is no

guarantee of future results. These investments may not be suitable for all

investors, and there is no guarantee that any investment will be able to sell

for a profit in the future. The Dow

Jones UBS Commodities Index is composed of futures contracts on physical

commodities. This index aims to provide

a broadly diversified representation of commodity markets as an asset

class. The index represents 19

commodities, which are weighted to account for economic significance and market

liquidity. This index cannot be traded

directly. The CBOE Volatility Index - more commonly referred to as

"VIX" - is an up-to-the-minute market estimate of expected volatility

that is calculated by using real-time S&P 500® Index (SPX) option

bid/ask quotes. VIX uses nearby and second nearby options with at least 8 days

left to expiration and then weights them to yield a constant, 30-day measure of

the expected volatility of the S&P 500 Index.

TIPS are U.S. government securities designed to protect investors

and the future value of their fixed-income investments from the adverse effects

of inflation. Using the Consumer Price Index (CPI) as a guide, the value of the

bond's principal is adjusted upward to keep pace with inflation. Increase in

real interest rates can cause the price of inflation-protected debt securities

to decrease. Interest payments on

inflation-protected debt securities can be unpredictable.

The NYCE US Dollar Index is a

measure that calculates the value of the US dollar through a basket of six

currencies, the Euro, the Japanese Yen, the British Pound, the Canadian Dollar,

the Swedish Krona, and the Swiss franc.

The Euro is the predominant currency making up about 57% of the basket.

Currencies and futures generally

are volatile and are not suitable for all investors. Investment in foreign exchange related

products is subject to many factors that contribute to or increase volatility,

such as national debt levels and trade deficits, changes in domestic and

foreign interest rates, and investors’ expectations concerning interest rates,

currency exchange rates and global or regional political, economic or financial

events and situations.

Corporate bonds contain elements

of both interest rate risk and credit risk. Treasury bills are guaranteed by

the U.S. government as to the timely payment of principal and interest, and if

held to maturity, offer a fixed rate of return and fixed principal value. U.S.

Treasury bills do not eliminate market risk. The purchase of bonds is subject

to availability and market conditions. There is an inverse relationship between

the price of bonds and the yield: when price goes up, yield goes down, and vice

versa. Market risk is a consideration if sold or redeemed prior to maturity.

Some bonds have call features that may affect income.

The bullish percent indicator (BPI) is a market breath

indicator. The indicator is calculated by taking the total number of

issues in an index or industry that are generating point and figure buy signals

and dividing it by the total number of stocks in that group. The basic

rule for using the bullish percent index is that when the BPI is above 70%, the

market is overbought, and conversely when the indicator is below 30%, the

market is oversold. The most popular BPI is the NYSE Bullish Percent

Index, which is the tool of choice for famed point and figure analyst, Thomas

Dorsey.