The Dow Jones Industrial Average (DJIA) gained 213 points (1.7%) last week pushing the DJIA up by nearly 650 points (5.3%) in the past two weeks. The S&P 500 added 1.3%, the Russell 2000 gained 0.3%, and the NASDAQ added 0.5% last week. Judging by these returns it is becoming apparent, in my view, that investors have been favoring the largest companies over smaller ones recently in a defensive move. For the year, the DJIA is up 4.5%, the S&P 500 is up 6.8%, the Russell 2000 is 4.1% higher, and the NASDAQ leads all major US indexes with a gain of 10.3%.

Europe remains under extreme duress and market volatility has picked up. For the week, the MSCI (EAFE) index, with its roughly 60% weighting to Europe, led all major indexes with a 2.2% increase on rumors that the European Central Bank (ECB), along with other central banks, were preparing to swoop in with an enormous bailout package and restore order to the markets. I believe that deep down, many European investors continue to believe a rescue will come, and they may be right. I have said repeatedly in this Update that it is in no one's interest to see the Euro and European Union (EU) collapse under the weight of Greece and related issues. For the year, the MSCI (EAFE) is now down 2.8%. The best performing international region is the Americas which includes the US, Canada, Brazil, Mexico, and four other Latin-America countries. The United States comprises 87% of the index giving further evidence to the strength of the US relative to the rest of the world.

Commodities in general have stabilized over the past two weeks. The Dow Jones UBS Commodity index was flat last week after increasing by 1.6% the week before. Oil prices continue to fall and a barrel of WTI Oil closed at $84.18. The last time oil prices have been this low was back in early October 2011. The Organization of Petroleum Exporting Countries (OPEC) announced last week that they would maintain current levels of production after Iran lobbied to cut production to raise prices on the eve of the Western-backed oil embargo targeting Iranian oil set to begin on July 1st. Lower prices reflect the decreased global demand and growing supply around the world. Gold prices rose $28.20 per ounce to close Friday at $1619.60 an increase of 1.8% from the previous Friday close. For the month, gold prices have climbed 3.4% on growing expectations the US Federal Reserve is likely to endorse some form of additional quantitative easing following a series of anemic US economic reports.

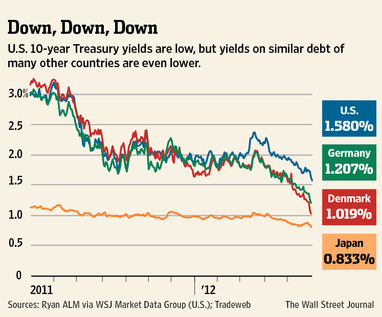

Bond markets here at home have remained on a slight but steady uptrend recently on the strength of US Treasuries. The yield on both 10 and 30-year Treasuries fell again to near historic lows closing Friday at 1.584% and 2.694% respectively. The US Barclays Aggregate US Bond index gained 0.3% last week and is up 2.5% for the year. The real story was in Europe with Spanish debt jumping dramatically last week to close Friday at 6.874%. This increase followed the announcement by the Spanish prime minister that his government had reached a deal for $125 billion in a direct banking bailout from the ECB and EU. Italian interest rates also increased, but at a much slower rate with the Italian 10-year yield closing the week at 5.926%. Most economists see 7% 10-year yields as the point where governments require a bailout. Spain is nearly there and Italy is closing in. Not to sound like a broken record, but I believe the Greek elections will have an enormous influence on these yields and I will be watching closely to see how they move into the new week. For the week, long-duration bond sectors were the best performing sector while short-duration and high yield were the weakest. For the year, preferreds, high yield munis, and extended duration treasuries have been the strongest bond sectors. Short duration and corporate high yield have been the weakest.

EUROPE IS IN TURMOIL

There is no other way to state it-Europe is in turmoil.

The first question to ask is what will happen to Greece? Will the country be immediately forced out of the Euro if the left-wing party, Syriza, is elected? Will Syriza be elected with enough of a majority to organize a government, or will the more moderate parties gain power? According to Richard Barley of the Wall Street Journal, it will not matter. He stated in his Heard on the Street column that in the end there will simply be more talks between the Greeks, the International Monetary Fund (IMF), and the European Commission. The Greek banking system is being kept afloat by the ECB and that would not likely change. Support by the ECB will become much more complicated, however, if the Greeks do decide to renege on their previous austerity commitments. A more balanced outcome, in my opinion, will be a little of everything. The European powers will soften their stance slightly on Greece and the Greeks will continue to shrink their economy and try to live within their means. Will this be a long-term solution? I doubt it, but it could have the effect of stabilizing the markets for a while in the weeks to come.

The next question is what will the world political leaders do? The G-20 has a scheduled meeting beginning on Monday in Mexico and Greece will certainly be topic number one. German Chancellor Merkel is coming under ever-increasing pressure from the Europeans and the US to soften her objections to a broad European mechanism to provide direct funding to European sovereign governments. Ms. Merkel sees this step, which would include the issuance of Euro Bonds (much like our Treasuries) by the ECB, as a violation of the EU charter and putting German taxpayers at risk on behalf of their many spendthrift neighbors. I believe President Obama will be pushing hard for greater spending because he does not want a full-blown economic crisis in Europe just months ahead of his re-election. In the end, I believe, they will talk a lot, issue statements citing their concern over what is happening, and speak of their determination to take whatever steps are necessary to get the crisis under control. Then they will all fly home.

So what happens Monday? Hard to say exactly. There may be some short-term volatility as investors react to the news, but I believe everyone will quickly begin to look at the real end game and that is what is going to happen to Spain and Italy. Liquidity is always the first and most critical problem that must be addressed. Money is the oxygen of the economic body, and I believe the ECB will step in as necessary as they have done before and provide liquidity to the European banks. The markets will breathe a sigh of relief and we will go back to watching the political leadership attempt to resolve the real problems. Those problems include a region that is in recession if not approaching depression in the southern tier countries, unsustainable levels of unemployment, and no appetite for real economic reforms. These reforms will need to include a more fiscally united Europe with governments surrendering part of their sovereignty, labor/union reforms, pension reforms, and a reduction of governmental spending as a percentage of their own gross domestic products (GDPs). If it sounds difficult, it is. There is no certainty that the EU will be capable of undertaking all of this without having to withstand further shocks to their economic systems. No one wins if the entire EU unravels into chaos, so expect the ECB and others step in to mitigate any crisis that emerges.

LOOKING AHEAD

As you know, I follow the technical data provided by Dorsey Wright & Associates (DWA) to help gauge my understanding of what is happening in the markets. My principal market indicator, the New York Stock Exchange Bullish Percent (NYSEBP), had its first positive week in 13 (going back to week of March 11-16). Additionally, several of my very short-term indicators have provided some positive indicators. However, the overall trend of the market is still negative and thus I remain cautious, but I have seen some signs of improvement. Additionally, both the DJIA and S&P 500 have moved from being oversold to about fair value.

Additional analysis about the current status of the markets provided by DWA show that US stocks clearly remain the favored investment of the five major asset categories. Bonds continue to hold the number two spot while Currencies, International stocks,and Commodities rank three, four, and five with International stocks and Commodities continuing to fall below cash on a relative strength basis. Within the US stock asset category, mid capitalization growth stocks are favored as are equal-weighted investments over capitalization-weighted indexes. Among the major economic sectors, relative strength analysis favors Consumer Discretionary, Information Technology, and Financials. Real Estate has fallen to fifth position behind Consumer Staples. One final note. The indicators I review in this paragraph are longer-term in nature. As I noted earlier, large capitalization stocks represented by the S&P 500 have slipped ahead of mid capitalization stocks on a short-term basis. I will continue to follow this trend very closely.

The NYCE US Dollar Index is a measure that calculates the value of the US dollar through a basket of six currencies, the Euro, the Japanese Yen, the British Pound, the Canadian Dollar, the Swedish Krona, and the Swiss franc. The Euro is the predominant currency making up about 57% of the basket.

Currencies and futures generallyare volatile and are not suitable for

all investors. Investment in foreign exchange related products is subject to many factors that contribute to or increase volatility, such as national debt levels and trade deficits, changes in domestic and foreign interest rates, and investors' expectations concerning interest rates, currency exchange rates and global or regional political, economic or financial events and situations.

Investments in commodities may have greater volatility than investments in traditional securities, particularly if the instruments involve leverage. The value of commodity-linked derivative instruments may be affected by changes in overall market movements, commodity index volatility, changes in interest rates, or factors affecting a particular industry or commodity, including international economic, political and regulatory developments.

Emerging market investments involve higher risks than investments from developed countries and also involve increased risks due to differences in accounting methods, foreign taxation, political instability, and currency fluctuation. The main risks of international investing are currency fluctuations, differences in accounting methods, foreign taxation, economic, political or financial instability, and lack of timely or reliable information or unfavorable political or legal developments.

The Dow Jones UBS Commodities Index is composed of futures contracts on physical commodities. This index aims to provide a broadly diversified representation of commodity markets as an asset class. The index represents 19 commodities which are weighted to account for economic significance and market liquidity. This index cannot be traded directly. The commodities industries can be significantly affected by commodity prices, world events, import controls, worldwide competition, government regulations, and economic conditions. Past performance is no guarantee of future results. These investments may not be suitable for all investors, and there is no guarantee that any investment will be able to sell for a profit in the future.

TIPS are U.S. government securities designed to protect investors and the future value of their fixed-income investments from the adverse effects of inflation. Using the Consumer Price Index (CPI) as a guide, the value of the bond's principal is adjusted upward to keep pace with inflation. Increase in real interest rates can cause the price of inflation-protected debt securities to decrease. Interest payments on inflation-protected debt securities can be unpredictable.

As always, if you have any specific questions on your portfolio or wish to talk to me, please do not hesitate to call.

Sincerely,

Paul Merritt, MBA, AIF ®, CRPC ®

Principal

NTrust Wealth Management

P.S. If you think this type of analysis would be of benefit to anyone you know, please share this communication with them.

Past performance is not indicative of future results and there is no assurance that any forecasts mentioned in this report will be obtained. Technical analysis is just one form of analysis. You may also want to consider quantitative and fundamental analysis before making any investment decisions.

Information in this update has been obtained from and is based upon sources that NTrust Wealth Management (NTWM) believes to be reliable, however NTWM does not guarantee its accuracy. All opinions and estimates constitute NTWM's judgment as of the date the update was created and are subject to change without notice. This update is for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of a security. Any decision to purchase securities must take into account existing public information on such security or any registered prospectus.

The bullish percent indicator (BPI) is a market breath indicator. The indicator is calculated by taking the total number of issues in an index or industry that are generating point and figure buy signals and dividing it by the total number of stocks in that group. The basic rule for using the bullish percent index is that when the BPI is above 70%, the market is overbought, and conversely when the indicator is below 30%, the market is oversold. The most popular BPI is the NYSE Bullish Percent Index, which is the tool of choice for famed point and figure analyst, Thomas Dorsey.

All indices are unmanaged and are not available for direct investment by the public. Past performance is not indicative of future results. The S&P 500 is based on the average performance of the 500 industrial stocks monitored by Standard & Poors, this is a market capitalization weighted index, meaning the largest companies in the S&P 500 have a greater weighting than smaller companies. The S&P 500 Equal Weighted Index is determined by giving each of the 500 stocks in the index the same weighting in the index. The Dow Jones Industrial Average is based on the average performance of 30 large U.S. companies monitored by Dow Jones & Company. The Dow Jones Corporate Bond Index is comprised of 96 investment grade issues that are divided into the industrial, financial, and utility/telecom sectors. They are further divided by maturity with each of the sectors represented by 2, 5, 10 and 30-year maturities. The Morgan Stanley Capital International (MSCI) Europe, Australia and Far East (EAFE) Index is a broad-based index composed of non U.S. stocks traded on the major exchanges around the globe. The Russell 2000 Index is comprised of the 2000 smallest companies within the Russell 3000 Index, which is made up of the 3000 biggest companies in the US.

Corporate bonds contain elements of both interest rate risk and credit risk. Treasury bills are guaranteed by the U.S. government as to the timely payment of principal and interest, and if held to maturity, offer a fixed rate of return and fixed principal value. U.S. Treasury bills do not eliminate market risk. The purchase of bonds is subject to availability and market conditions. There is an inverse relationship between the price of bonds and the yield: when price goes up, yield goes down, and vice versa. Market risk is a consideration if sold or redeemed prior to maturity. Some bonds have call features that may affect income.

Securities and Advisory Services offered through Commonwealth Financial Network®,

Member FINRA/SIPC, a Registered Investment Adviser.